What was the Angel Tax?

The Angel Tax came into play if the total investment value exceeds the company's FMV or Fair Market Value. Investment greater than FMV is categorized as "income from other sources", and the tax imposed on it is called angel tax. The tax was first introduced in the 2012 Union Budget by then finance minister Pranab Mukherjee to arrest the laundering of funds.

This was a unique tax as it converted Capital receipts to Income and taxed Founders and Investors. It adversely impacted the Indian start-up ecosystem by diminishing investors' ability to take commercial risks.

For example, if a company's fair value is Rs 1 crore and it raises Rs 1.5 crore from angel investors, the excess amount of Rs 50 lakh is subject to this tax. Tax authorities considered the premium paid by investors as income, taxable at around 31 percent.

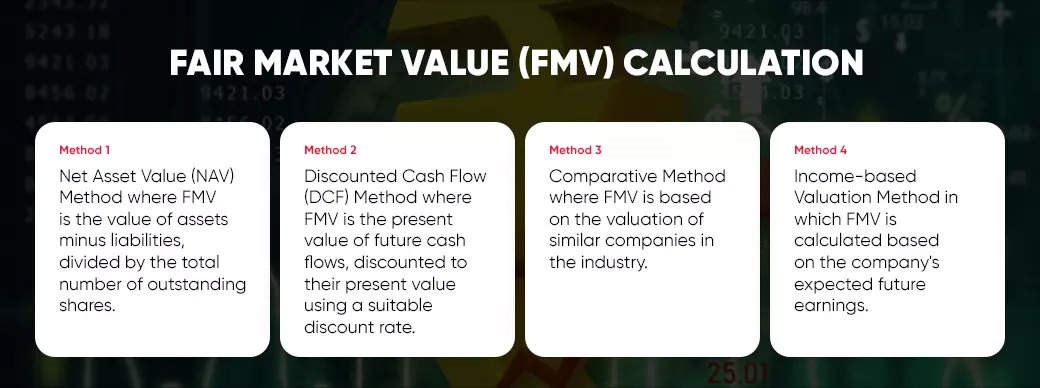

Methods of ascertaining FMV:

The issue with these approaches is that they do not apply to Early-stage companies. This led to friction for Founders & Investors as they struggled to complete formalities and even faced litigation in some cases.

We have spoken about why Valuing early-stage startups is difficult here..

The sequence of events:

2012:

The Angel Tax was introduced as part of the Finance Act of 2012. Placed under the Income Tax Act of 1961, the rationale was to curb money laundering and Tax evasion using Private market investments.

From 2016 to 2018, Angel Funds significantly dried up and the number came down by more than 40%.

2019:

After startups made numerous pleas, the Indian Government implemented some relaxations in the 2019 Union budget. In this budget, the government stated that if the startup is registered under the DPIIT or Department for Promotion of Industry and Internal Trade, it would not be subject to such tax. But these relaxations were still subject to fairly strict guidelines such as:

· After issuing the shares, the startup's maximum paid-up capital and share premium should not exceed Rs 25 crore.

· As per Rule 11 UA (2)(b) of the Income Tax Act of 1961, it is imperative for the merchant banker to evaluate the fair market value of the startup.

· These relaxations did not help reduce frictions regarding reporting or legal tasks & hence was not a welcome move.

2024:

Even after numerous incentives, the complaints regarding Angel Tax were never resolved. As a result, the Union Government took the significant step of eliminating the concept of 'Angel Tax' in the 2024-25 Budget.

What changes with the Abolishment of Angel Tax?

· Simplification of the Fund-raising process with reduced bureaucracy

· Encouraging Foreign investment as well due to reduced scope of Tax litigation

· The fiscal discipline demonstrated by startups after the funding winter has made the Indian eco-system more attractive for Investors

Conclusion:

The removal of the Angel Tax is a welcome move for the start-up ecosystem. Due to the reduced tax and regulatory hurdles, we can expect a more dynamic landscape for investments in India.

The provisions through which angel tax is imposed will cease to be in force from April 1, 2025.