Realities of next round financing

In the last 2 quarters, we have had a handful of conversations with portfolio companies for funding. These companies can be categorized broadly into the following buckets:

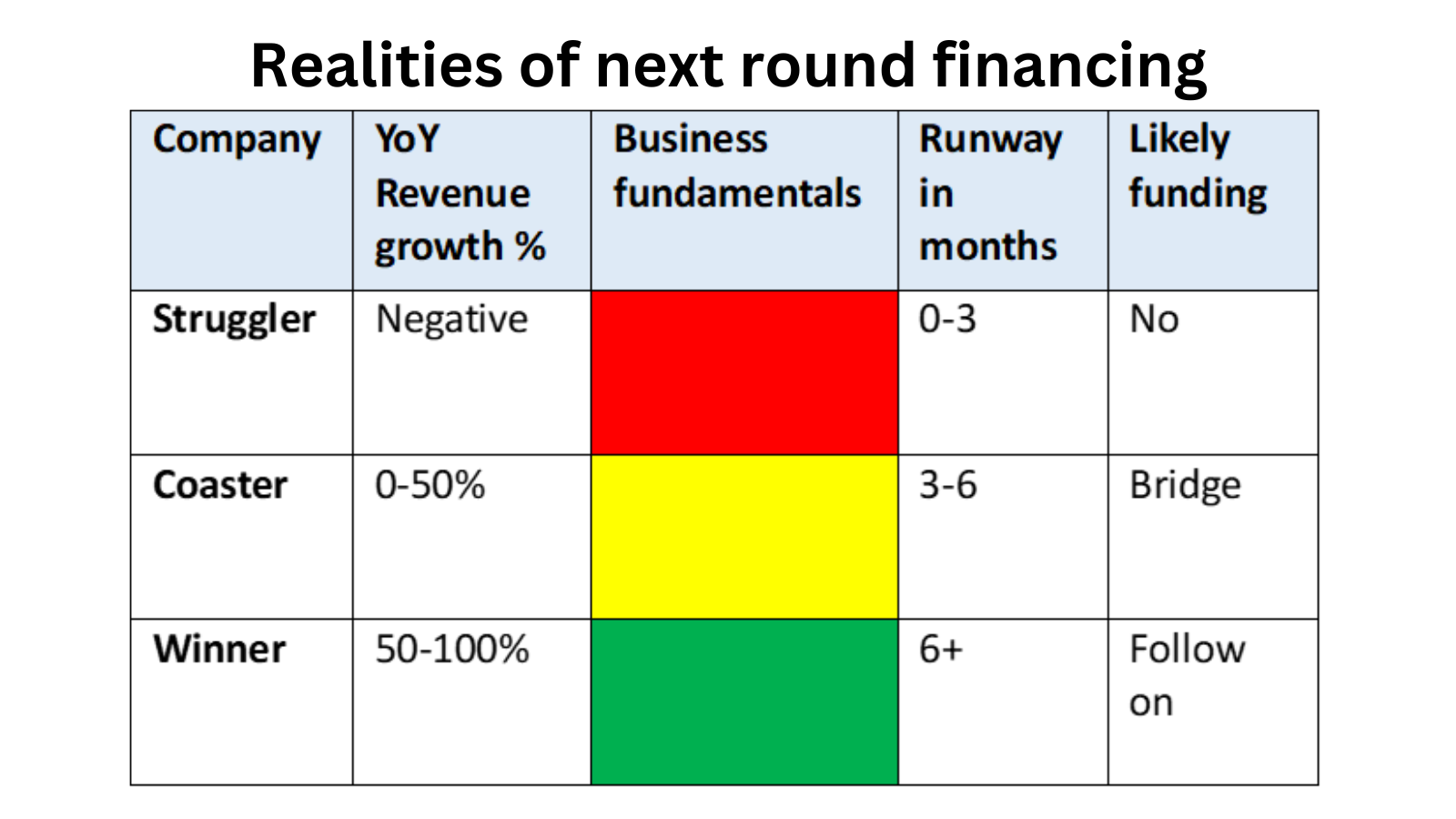

STRUGGLER

Meaning: A struggler is a company which has seen revenue degrowth in the past 12 months and its core business fundamentals are on shaky wicket

Key point: These companies could not validate their initial business hypothesis, or got out-competed by their peers. Strugglers typically fail to reinvent themselves and are unable to find the next hypothesis to validate in order to prove milestone achievement for their next round of financing

Typical conversations: “We will break even in the next quarter if X happens, and we need emergency funding to do that”

Investor point of view: As investors, it is very difficult to justify additional funding to strugglers in the absence of either a) new business definition or hypothesis, or b) visibility of strong growth in existing business

Likely outcome: Investors will typically pass and companies may shut down

COASTER

Meaning: A coaster is a company which has seen some revenue growth over the past 12 months and its core business fundamentals are steady – neither improving nor deteriorating

Key point: These companies validated their initial business hypothesis but could not excel in their traction or growth. Coasters by definition coast along where the market takes them. They are on the fence, with investors wanting to see evidence of them becoming winners in the future before they make up their minds to invest

Typical conversations: “We are doing well with evidence of sales growth; we have some cash in bank but we need more funding soon in order to go all out and achieve milestones required for the next round”

Investor point of view: New investors rarely do bridge rounds to support a non-portfolio company. Existing investors are open to supporting a bridge only if they see evidence of growth, good and constant communication & data to prove & disprove the founders’ hypothesis

Likely outcome: Depending on growth, and comfort level with founders, existing investors may participate with small cheques in order to support cash burn and milestone achievement to enable companies to raise their next round. Typically, convertible structures are used with a cap, floor, and discount to price of next round

WINNER

Meaning: A winner is a company which has seen strong revenue & traction growth over the past 12 months and its core business fundamentals are improving

Key point: These companies validated their initial business hypothesis and excel in their traction or growth. Winners typically meet or outperform their milestones of previous round. There is evidence that the company is in the right direction

Typical conversations: “We have met/exceeded milestones and are ready to raise our next round”

Investor point of view: These companies have strong interest from multiple investors (new & existing). Typically existing investors are happy with the performance and provide an initial soft commitment of 20-30% of the target round while the founder brings in a lead investor who takes up a majority

Likely outcome: These companies are able to raise from multiple investors and close their round from a place of abundance before their cash runs out

Facing the realities

Understanding the realities of next-round financing is crucial. Strugglers face challenges in validating their business hypothesis, while coasters need to demonstrate potential for investor interest. Winners with strong revenue and traction have multiple funding options.

Regardless of your category, take proactive steps to strengthen your position. Analyze your business hypothesis, seek feedback, and communicate transparently with investors. Strugglers and coasters should focus on reinventing themselves or finding new growth avenues. Winners should secure commitments from existing investors and seek a lead investor.

In conclusion, assess your position honestly, adapt your strategy, and take proactive steps to secure the funding you need.