BluSmart and Gensol - A Lesson in Frugal and Patient Capital

As a venture investment firm advocating for frugal capital and patient capital, we have seen many startups rise with promise only to falter under the weight of mismanaged ambition. The intertwined story of BluSmart Mobility and Gensol Engineering offers a compelling case study. Once heralded as pioneers in India’s green mobility and renewable energy sectors, these companies are now mired in financial distress as of April 8, 2025. This blog explores BluSmart’s origins, its founders’ vision, the roots of their financial troubles, and whether haphazard capital spending derailed their journey. For startups seeking venture capital or sustainable investing, this tale underscores the importance of disciplined growth.

How BluSmart Started

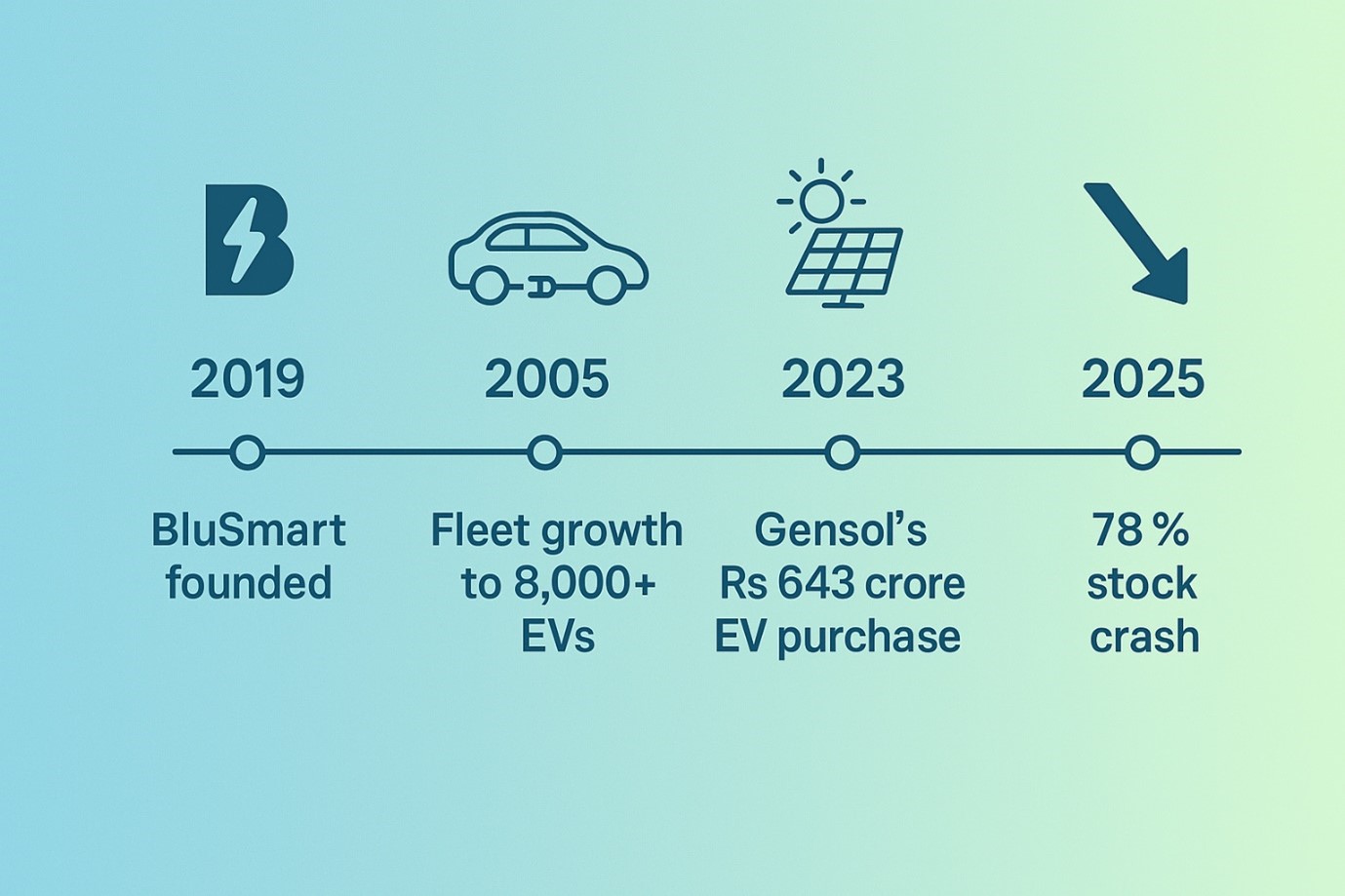

BluSmart Mobility launched in 2019, founded by Anmol Singh Jaggi, Puneet Singh Jaggi and Punit Goyal. The trio aimed to disrupt India’s ride-hailing market—dominated by Uber and Ola—with an all-electric vehicle (EV) fleet, positioning BluSmart as a sustainable alternative. Anmol and Puneet, brothers with a background in renewable energy through their listed venture Gensol Engineering (founded in 2007), brought technical expertise, while Punit Goyal, a serial entrepreneur, added business acumen from his prior ventures in solar energy.

The startup emerged from a synergy with Gensol, which initially focused on solar engineering, procurement, and construction (EPC). Gensol’s diversification into EV leasing provided BluSmart with its initial fleet, a move that seemed strategic at the time. Backed by over $200 million from investors like BP Ventures, BluSmart scaled rapidly, reaching a fleet of 8,000+ EVs by 2025 and operating in Delhi-NCR and Bengaluru. Its vision? To make EV ride-hailing accessible across India within a decade, as Anmol boldly stated in early 2025.

In the Limelight: Founder on Nikhil Kamath’s Podcast

In December 2023, Punit Goyal appeared on Nikhil Kamath’s “WTF is with Nikhil Kamath” podcast, episode titled “WTF is Happening with EV?”. Joined by EV industry peers, Punit shared BluSmart’s origin story and his entrepreneurial journey. He recounted how his dissertation at Aston University sparked a passion for clean energy, leading him to establish PLG Power, a solar panel manufacturing venture. This evolved into a 20 MW solar plant in Gujarat, sold for $68 million to a Saudi firm, and a 70 MW plant in Maharashtra, sold to Suzlon for $55 million. These successes introduced him to Anmol Jaggi, whose Gensol built the Gujarat plant in a record four months.

Punit framed BluSmart as a natural progression of his clean energy ethos, emphasizing its potential to transform urban mobility. The podcast showcased the founders’ confidence and ambition, resonating with investors and enthusiasts alike. However, it also hinted at a reliance on bold moves—like leveraging Gensol’s resources—without fully addressing the risks of such interdependence.

Why the Financial Troubles?

By April 2025, BluSmart and Gensol faced a cascading crisis. Gensol’s stock had plummeted 78% year-to-date, hitting a 52-week low of Rs 166.30, while BluSmart scaled back operations and lost key executives. Several factors fueled this downturn:

1. Debt Overload at Gensol: Gensol amassed significant debt—Rs 470 crore owed to IREDA alone by late 2024—to fund its EV fleet for BluSmart. When credit agencies ICRA and CARE downgraded Gensol to default status in March 2025, citing delayed debt servicing and alleged falsified documents, its financial flexibility evaporated.

2. Failed Asset Sale: Gensol attempted to offload 2,997 EVs (37% of BluSmart’s fleet) and Rs 315 crore in debt to Refex Green Mobility. The deal collapsed in March 2025 due to the EVs’ poor condition and BluSmart’s refusal to accept higher lease rates, leaving Gensol’s debt reduction plan in tatters.

3. Leadership Exodus: BluSmart’s CEO Anirudh Arun, CTO Rishabh Sood, CBO Tushar Garg, and VP Priya Chakravarthy exited in March 2025 amid restructuring efforts, signaling internal turmoil.

4. Market Pressure: Competitors like Rapido encroached on BluSmart’s turf, poaching drivers with incentives, while daily rides dropped from a peak of 25,000-30,000 to under half that number.

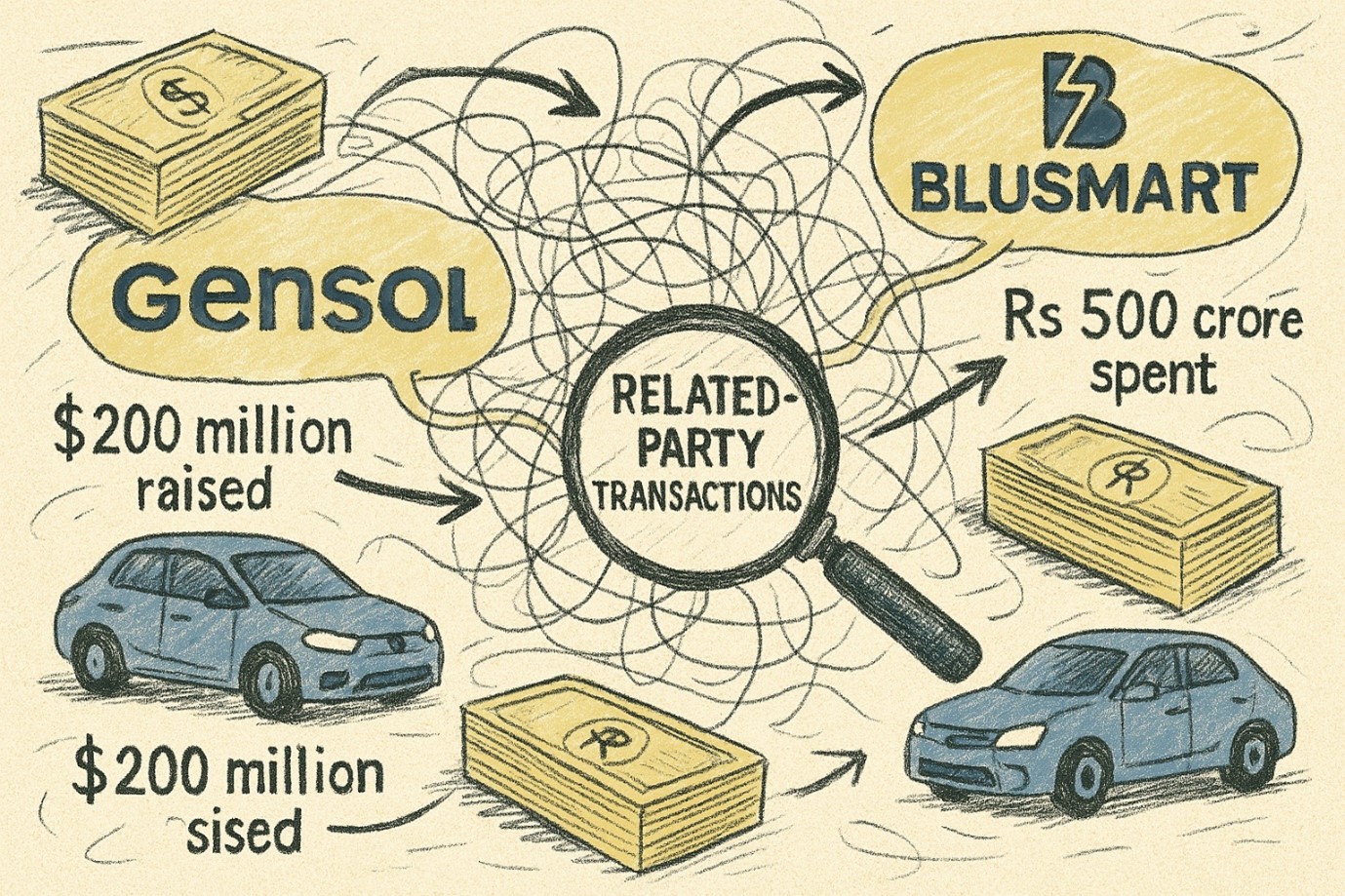

5. Governance Concerns: Allegations of related-party transactions between Gensol and BluSmart raised red flags. Gensol’s FY24 report disclosed Rs 148 crore in contracts with BluSmart subsidiaries, prompting scrutiny over transparency and shareholder fairness.

6. These issues reveal a classic pitfall: over-reliance on a single partner (Gensol) and aggressive expansion without a sustainable financial foundation.

Was the capital strategy reckless?

BluSmart and Gensol’s capital allocation offers a stark lesson in frugal capital mismanagement. Gensol raised Rs 643 crore in 2023 from Power Finance Corp to buy 5,000 EVs, primarily for BluSmart, and spent over Rs 500 crore in FY24 supporting its sister company. BluSmart, meanwhile, burned through its $200 million war chest to build a capital-intensive model—owning or leasing its fleet and charging infrastructure, unlike Uber’s asset-light approach.

Was this haphazard? Consider:

- Leasing thousands of EVs from Gensol locked both companies into a high-cost structure. When Gensol’s liquidity faltered, BluSmart couldn’t pivot, losing fleet access and operational agility.

- BluSmart’s fleet relied heavily on Gensol (two-thirds of its EVs), ignoring risks of single-source dependency. Contrast this with a frugal approach: phased growth with multiple suppliers.

- Expansion into Dubai (shuttered in 2025) and plans for an IPO diverted focus from profitability and screams of premature scaling, which Punit Goyal admitted was 6-8 quarters away as late as March 2025

- The Gensol-BluSmart nexus, including discounted leases, suggests capital was funneled without clear ROI, eroding trust and financial stability.

This wasn’t just ambition—it was reckless overreach. A patient capital strategy would have prioritized profitability over scale, testing the model in one market before piling on debt and assets.

Wait – there is little more

BluSmart never revealed clear unit economics. Some known issues:

- Utilization of EVs dropped in 2024–25

- Charging and maintenance costs remained high

- Customer subsidies may have temporarily propped up ridership

Without strong recurring revenue, the capital burn became unsustainable—even with $200M in funding.

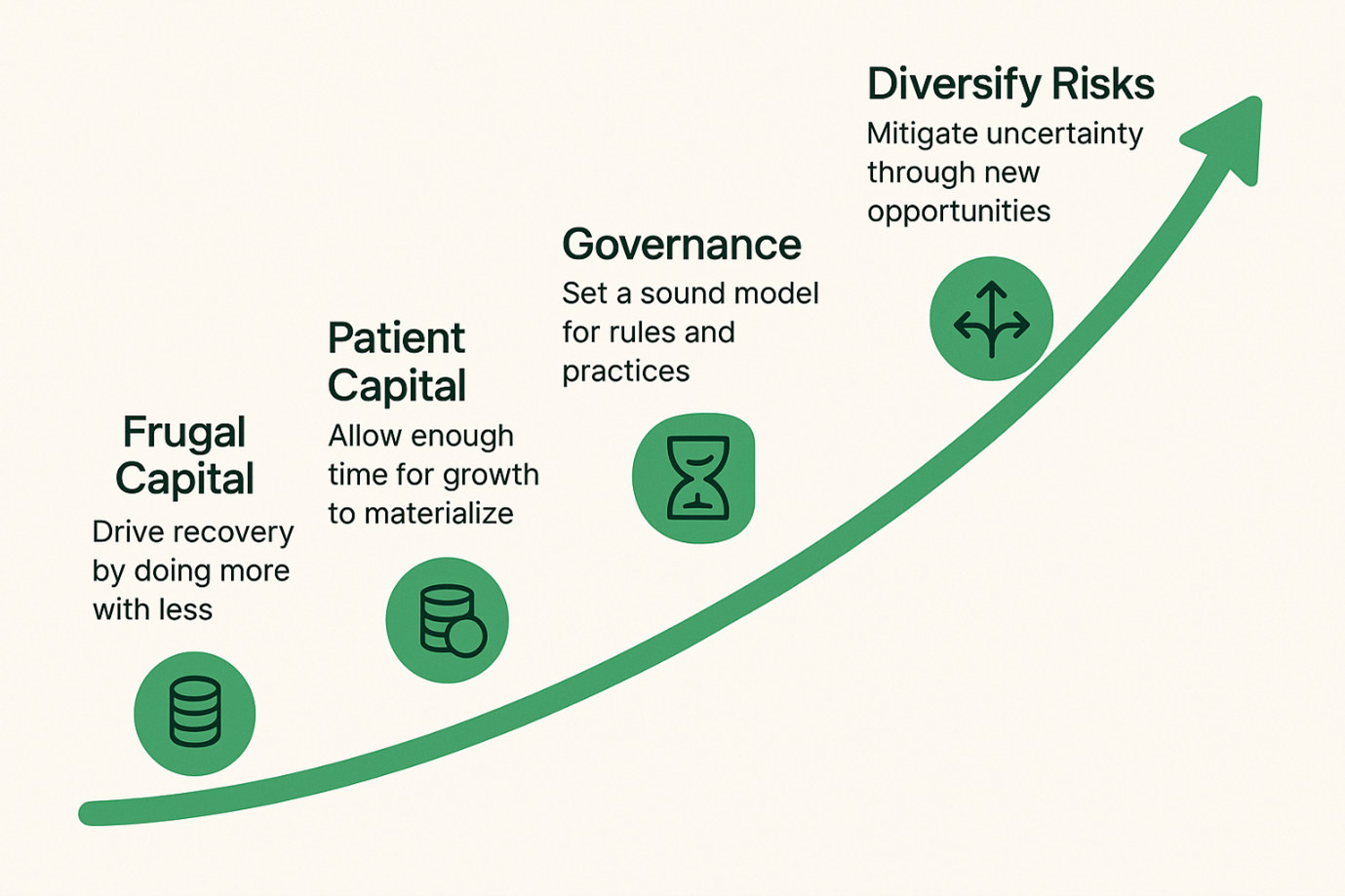

Lessons for Startups and Investors

As a firm championing sustainable investing, we see BluSmart and Gensol as a cautionary tale:

1. Frugal capital wins:

Build lean, validate demand, and scale incrementally. BluSmart’s asset-heavy model consumed cash without proving unit economics.

2. Patient capital pays off:

Resist the rush to unicorn status. Gensol’s debt-fueled growth and BluSmart’s premature expansion sacrificed long-term resilience.

3. Governance matters:

Transparency with investors and regulators is non-negotiable. Opaque dealings eroded confidence in both companies.

4. Diversify Risks:

Dependency on a single partner or supplier can sink even the best ideas. BluSmart’s fate hinged too much on Gensol.

For companies seeking startup funding, this case study is a roadmap.

Partner with investors who value discipline over hype—those who see growth as a marathon, not a sprint.

The road to success isn’t paved with borrowed billions—it’s built with deliberate, sustainable steps. Let’s fund the future responsibly.